Why European SaaS Companies Struggle to Reach $100M ARR

The 75x valuation gap explained—and how to close it while keeping European advantages

When Pipedrive's founders started building their CRM in a small Tallinn office in 2010, they had one obsession: making sales pipeline management so intuitive that sales reps would actually love to use it. Fast-forward to today, and they've largely succeeded. Pipedrive consistently ranks at the top of user satisfaction surveys, boasts industry-leading adoption rates within sales teams, and has expanded to serve over 100,000 companies worldwide. Users routinely praise its clean interface, logical workflow, and refreshing lack of feature bloat.

Meanwhile, 3,000 miles west, Salesforce, a platform that many sales professionals openly complain about using, commands a market cap of over $200 billion. Pipedrive, despite its superior user experience and impressive growth trajectory, was valued at only $1.5 billion when Vista Equity Partners acquired it in 2020.

This isn't just a story about two CRM companies. It's a perfect illustration of the European SaaS paradox: we're building products that users genuinely love and prefer, yet somehow missing the unicorn valuations that seem to flow effortlessly to the Silicon Valley counterparts. The question isn't whether European SaaS companies can build world-class products—Pipedrive, Linear, and Loveable, along with dozens of other European success stories, prove we can. The question is why the market doesn't seem to care.

To understand this paradox, we need to examine both the reality of European SaaS competitiveness and the structural forces that create this valuation gap.

The Evidence: European SaaS Quality vs. Market Reality

In March of this year, I conducted a comparison between SaaS companies in the US and Europe and discovered that, for instance, the payback period of customer acquisition, revenue per employee, and median efficiency are comparable. Given the lower valuation, it should also be a sign that the businesses' quality is inferior to that of the US, but that research told a different story.

The other factor is the customer preference. The European products, like Pipedrive, Linear and Loveable, are commonly praised for their clean usability compared to the market leaders in their categories. The usability and ease of implementation are valued by the smaller and midsize companies, which Europe is full of. The enterprise segment is frequently the focus of US companies from the start, which makes products often more difficult to use and implement but does, when implemented properly, produce more value.

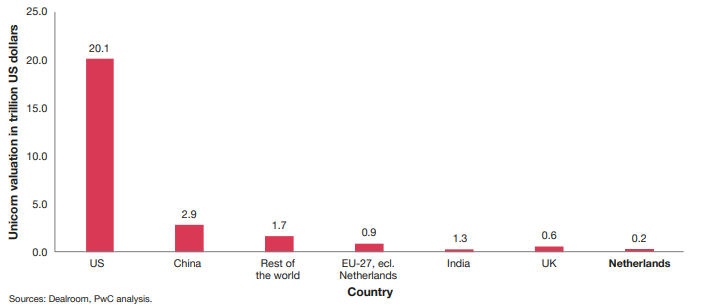

Even though European companies are competitive, particularly in the SMB market, US unicorns make up 75% of the global unicorn value, while European unicorns only make 1% (see the image below from PwC Research).

The 75x Gap: Four Reasons Europe Lags Behind

We can all probably agree that the volume of tech companies in the US is much higher, so their combined valuation should be higher. However, why is the valuation seventy-five times higher? I believe there are four reasons behind this: market, growth, capital and talent.

Market Size: Europeans target first their home market, which is significantly smaller than the US home market of 330 million. Starting to export requires always adapting to language and cultural differences, which are time- and resource-consuming.

Growth philosophy: Founders in Europe often aim for sustainable growth, while US founders have the growth-at-all-costs mentality. Compared to Americans, Europeans are therefore more risk averse and strive to avoid failure. A failure is viewed more negatively over here, and successful business in Europe starts at a much lower level than in the US.

Access to capital: Although the European venture capital ecosystem has seen positive developments, it still was only $51 billion in 2024, or 25% of the total amount of VC money invested in the US. An interesting side fact is that the rate of return in Europe is higher than in the US (20.8% vs 18.9%, Invest Europe).

Talent availability: Last but not least, building requires top talent. American businesses pay more, and taxes are simpler and less complicated in the US, particularly when it comes to options and equity. When hiring the best talent in the world, this is a definite advantage.

Europe's Hidden Competitive Advantages

Should we simply accept Europe's 1% share of global unicorn value and concede defeat? Or does Europe have hidden advantages that would make it a good place for unicorns to live? Undoubtedly, it does. Consider, for example:

Regulatory Readiness: European companies build privacy-first from the start. While this is a burden, it is also an advantage, as privacy standards and regulations have spread globally.

Efficient Capital Usage: Lower cost of talent also means lower burn rates, longer runways, and more sustainable unit economics. They help you get farther with the same investments if you find good talent.

Global Market Understanding: Better positioned for international expansion due to multicultural experience. Since the home market is small, starting to export is a must, and the knowledge of the nuances of different cultures is a strong advantage.

Clean Design. When done correctly, we do have an advantage when we concentrate on designing for great usability. The catch is that you need to be 10x better than the established competitors.

Linear exemplifies this approach perfectly—they combined European design excellence with global ambition, building a product development tool so intuitive it converts users from Atlassian, the de facto tool for all product teams, while raising their Series C at a $1.25 billion valuation.

The Path Forward: Turning Disadvantages into Strengths

So there is hope, but it requires a fundamental shift in mindset. European founders need to stop seeing their constraints as limitations and start leveraging them as competitive advantages.

Mindset Shifts: Think Global, Build European

The most successful European SaaS companies succeed by combining European design sensibilities with global ambition. This means:

Start with global markets in mind, not just your home country

Use your design advantage to build products that are 10x better, not just incrementally better

Embrace sustainable growth as a feature, not a bug—longer runways mean you can outlast venture-backed competitors during downturns

Strategic Positioning: Lead with Strengths

European companies should position themselves as the "premium, privacy-first alternative" rather than the "cheaper option". This means:

Privacy as a product feature, not just compliance

Efficiency as innovation—show how you deliver the same results with less complexity

Quality over quantity—target customers who value craftsmanship over feature bloat

Capital Strategy: Beyond Traditional VC

The European funding gap isn't just a problem—it's an opportunity to build more sustainable businesses:

Revenue-based financing for profitable, growing companies

Strategic partnerships with established European enterprises

Government grants and EU funding for deep-tech innovation

Customer-funded growth through premium pricing strategies

The companies that master these alternative approaches won't just survive—they'll be antifragile when the next funding winter hits.

The European Advantage is Real

What if the European approach isn't the problem but the preview of where the entire SaaS industry is heading? As markets mature, customers increasingly value privacy, sustainability, and user experience over growth-at-all-costs. European companies are already optimised for this future.

The question isn't whether Europe can build unicorns—it's whether we're brave enough to define success on our own terms while still thinking big enough to matter globally. The European SaaS industry stands at an inflection point. We have the talent, the advantages, and increasingly, the examples of success. What we need now is the courage to think as big as our American counterparts while staying true to the principles that make European products exceptional.